would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

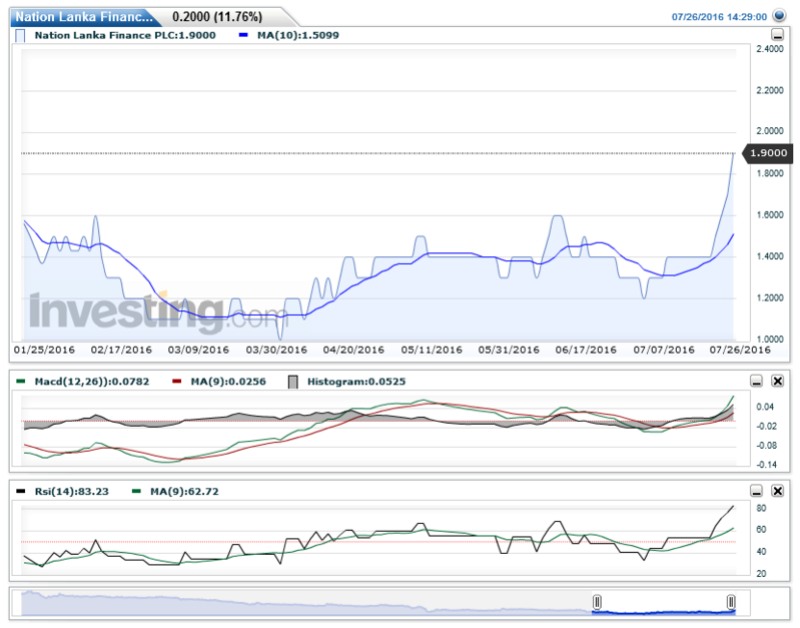

Nation Lanka, hammered with impairments and deposit withdrawals following Golden key saga, is recovering slowly yet steadily. Their new business model has earned them a fantastic interest yield with a huge loan book growth. As some of you may aware now Nation Lanka has entered into the lucrative micro finance business and join hands with COCR, BIL and LOFC.

Just a summary of key financials with a conservative estimate for FY 2016/17 is given below.

According to the above table you may seen the double digit growth in loans and advances with an interest yield of over 40%, a mark achieved by none other than BLI. You may recall my thread on benchmarking finance sector stocks where I showed BLI earning an interest yield of over 48% where as majority of other finance companies just generate a yield around 20%-25%. So in that sense you can get an idea as to how Nation Lanka will do in the future.

The above PAT was estimated based on very conservative assumptions of loan book growth and PAT margins yet they can generate an EPS of 30 cents for the next financial year which translates to a PE of 6x at the closing price of Rs1.8 but still trading at a discount to the industry PE benchmark. NAV tyrned to positive 1 in 15/16 from a negative 1 in 14/15.

So within 2 to 3 years this company generating a profit in excess of half a billion so that the price should reach Rs5/- which means a lucrative medium term investment for you.

Do your own analysis also to take an informed decision.

Thanks

Just a summary of key financials with a conservative estimate for FY 2016/17 is given below.

| Rs mn | 2014/15 A | 2015/16 A | 2016/17 F |

| Loans & Advances | 4389 | 5608 | 7,080 |

| Growth in loans & advances | 64% | 28% | 26% |

| Interest income | 1165 | 2087 | 2,780 |

| Growth in interest income | 29% | 79% | 33% |

| Interest yield | 33% | 42% | 44% |

| NPAT | -429 | 162 | 222 |

The above PAT was estimated based on very conservative assumptions of loan book growth and PAT margins yet they can generate an EPS of 30 cents for the next financial year which translates to a PE of 6x at the closing price of Rs1.8 but still trading at a discount to the industry PE benchmark. NAV tyrned to positive 1 in 15/16 from a negative 1 in 14/15.

So within 2 to 3 years this company generating a profit in excess of half a billion so that the price should reach Rs5/- which means a lucrative medium term investment for you.

Do your own analysis also to take an informed decision.

Thanks