would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

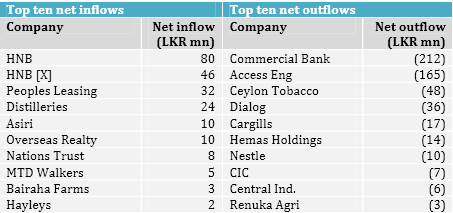

Latest*

Latest*

What is the most affected banking sector share?

In my opinion its NTB. Why I say so?

They have a staggering 25% of leasing out of loans to customers...

In my opinion its NTB. Why I say so?

They have a staggering 25% of leasing out of loans to customers...