would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

Strong demand for air travel amidst heightened macroeconomic risks

Airports Council International (ACI) World has published its eleventh quarterly assessment analyzing the impact of the COVID-19 pandemic, its effects on airports, and the path to recovery.Despite strong headwinds, the industry is continuing to recover as more countries ease travel restrictions and open their markets, including Japan in the Asia-Pacific region. This coupled with the propensity for air travel will drive the industry’s recovery, expected to reach 2019 levels in 2024.

Macroeconomic risks

As the world emerges from the worst health crisis of modern times, the global economy faces a new array of challenges. From the ongoing conflict in Ukraine to bottlenecks in global supply chains, there are risks that threaten to disrupt the pace of the post-pandemic recovery. The most obvious manifestation of such risks is the significant increase in prices for different sectors, particularly food and energy. This sudden rise in cost has in turn produced a tightening of global monetary policy, with central banks increasing interest rates to tame inflation. This will inevitably cause a decrease in economic activity and potentially impact consumer confidence.

Contributing to these inflationary pressures is a tight labour market across many jurisdictions. The shortage is especially felt in the air transport sector where stakeholders across the entire aviation ecosystem moved from a weakened state of demand due to travel restrictions earlier in the year to an immediate surge in demand with the lifting of restrictions. Matching available capacity and human capital with that strong surge in demand in such a short period of time remains a challenge. In essence, there are macroeconomic pendulums moving in opposite directions that are affecting air transport demand. Though higher input prices will inevitably impact the cost of travel, unemployment rates remain historically low with continued pent-up demand for air travel. Low levels of unemployment in the broader population and rising real incomes increases the propensity to travel. However, some analysts argue that this may be short lived as central banks continue to tame inflation with higher interest rates, thereby contracting economies—the heightened downside risk of a recession that is characterized by both a contraction in output and higher unemployment levels remains omnipresent on the horizon. If this risk materializes, it could represent an important headwind for air transport on its path to recovery in major aviation markets.

A strong yet uneven recovery in H1 2022 airport passenger traffic

The recent momentum created by the lifting of many health measures and the relaxation of most travel restrictions in many European countries and in the Americas has renewed industry optimism. It however exposed even more the uneven recovery—a notable gap exists among markets, especially where COVID-19 vaccine availability and uptake are limited, geopolitical conflicts are visible, or strict travel restrictions are still enforced. This gap resulted in offsetting the impact of pent-up demand during the early Northern Hemisphere summer season on a global scale. For instance, major aviation markets in Asia-Pacific lagged behind their North American and European counterparts as they imposed restrictive measures for international passenger traffic especially through the lens of the first half of 2022—H1 2022 versus H1 2019. The Asia-Pacific markets of Japan at 39% of H1 2019 levels in the first half of 2022, Thailand (31%) and China (28%) were all well below pre-pandemic levels. On the other hand, markets like Colombia, Mexico and Nigeria welcomed a surge in demand and exceeded their 2019 levels. The United States (87% of 2019), Spain (82%), Brazil (80%), and India (75%) were among other major aviation markets also making strides to close the gap with 2019 passenger levels in the first half of 2022.

Despite the heterogenous recovery, air travel should see a continued uptick on the aggregate in the second half of 2022, moving the industry closer to its recovery. While many indicators are pointing towards the recovery, the industry is also facing some noteworthy headwinds.

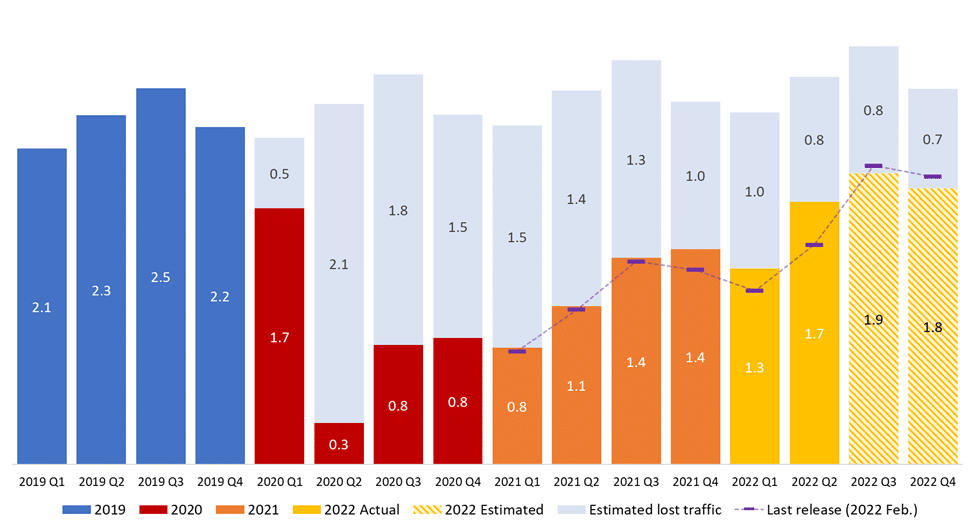

Chart 1: Projected global quarterly passenger losses due to the COVID-19 crisis (2019–2022, in billions of passengers)

- With the global passenger volumes for the full year 2021, compared to the projected baseline (the pre-COVID-19 forecast for 2021) of 9.8 billion passengers, it is estimated that the COVID-19 outbreak reduced traffic by 5.2 billion passengers, representing a potential loss of 52.9%. The attributed loss would be 49.5% when compared to the 2019 results, representing a loss of 4.5 billion passengers (from 9.2 billion passengers in 2019).

- During the first two quarters of the year 2022, global passenger volume was 1.3 billion and 1.7 billion, which are 62.0% and 75.2% of 2019 levels. Compared to the projected baseline, the estimated traffic losses represent a loss of 44.4% and 32.2% respectively, reducing the gap faster than the last estimation of the ninth quarterly assessment, released in February 2022.

- The recovery was mainly driven by the sudden surge of air travel demand during the Northern Hemisphere summer of 2022, following the relaxation of travel restrictions, which was higher than expected demand.

- The Latin America-Caribbean region had the strongest first half of 2022 among regions, bringing the region to report declines of 23.7% and 14.9% for 2022 Q1 and Q2 compared to the projected baseline (84.6% and 94.9% of 2019 level).

- The North America region marked the second highest, however, slowed down compared to the fast-recovering trend in the year 2021, with its traffic down 27.1% and 17.3% for 2022 Q1 and Q2 compared to the projected baseline (79.6% and 89.8% of 2019 level).

- The most significant jump in 2022 Q2 was observed in Europe, driven by the Northern Hemisphere summer travel demand surge, with 42.1% and 21.9% below the projected baseline for 2022 Q1 and Q2 (63.0% and 83.5% of 2019 level).

- With significant improvement in 2021 Q4, the Middle East region continued its recovery in 2022 Q1 and Q2, losing 39.5% and 28.0% of its passenger traffic for the year compared to the projected baseline (72.0% and 84.2% of 2019 level).

- Africa also recorded gains, albeit lower than global levels, with declines of 44.4% and 36.1% for 2022 Q1 and Q2 respectively, compared to the projected baseline (70.2% and 80.2% of 2019 level).

- In contrast to early recovery in the first half of the year 2021, Asia-Pacific showed the least improvement in 2022 Q1 and Q2, with 59.7% and 52.4% below the projected baseline (45.3% and 54.1% of 2019 level).

Chart 2: Projected global quarterly passenger traffic compared to 2019 level (2021-2022, indexed, 2019 Level = 100%)

Source: ACI World

Table 1: The impact of the COVID-19 crisis on quarterly passenger traffic by region (2021 and 2022, rounded to nearest million passengers)

* Estimated passenger traffic volumes are based on a broad range of inputs provided by ACI Regional offices and industry experts.

** The projected baseline (pre-COVID-19) scenario is based on a standard time-series forecast generated using the most up-to-date and complete historical data to August 2022. It also makes use of an adjusted World Airport Traffic Forecasts (WATF) 2019–2040 and considers the latest insights provided by ACI Regional offices and other inputs.

Source: ACI World

The outlook and road to recovery

Uncertainty still surrounds the recovery of the aviation industry, especially in the medium-term. Projecting the path to recovery at this point is still an exercise requiring prudence. The potential for an economic downturn and possible recession continues to increase in probability. Those risks could dampen or delay the recovery. Adding to the uncertainty is the ongoing geopolitical conflicts in Eastern Europe and related humanitarian crises. Weaker vaccination rates in emerging and developing countries and the risk of a northern hemisphere fall/winter outbreak globally may also represent further headwinds.

The speed of the recovery still depends heavily on a number of stakeholders and the level of coordination pursued by national governments across the globe. With the removal of travel restrictions and quarantine requirements for vaccinated travellers in the first half of 2022, there has been an upsurge in demand. Despite a number of headwinds, the baseline projections indicate that the industry as a whole will recover to 2019 levels by the end of 2023 or in early 2024. The recovery of the sector to pre-COVID-19 levels is expected to be driven mainly by domestic travel, which is projected to recover to 2019 levels by 2023. International travel is forecast to recover by 2024. Both the upside risks that act to stimulate demand as well as the downside risks that will curb demand are listed below:

Upside risks

- Pent-up demand and historically low unemployment rates in major economies

There are clear signs of a surge in air travel demand resulting from a combination of low unemployment rates, accumulated savings by consumers during the pandemic, vacation deprivation felt by many leisure travellers, and the desire to reconnect with families, friends and/or colleagues. Many industry analysts refer to it as “revenge travel,” as passengers rush to take to the skies after being homebound for the last two years.

- Strong vaccination rates and relaxation of travel restrictions

The easing of travel restrictions, a major hurdle to air transport and international traffic in particular, increases the demand for air travel. Most countries in all regions have plans to lift many, if not all, health measures, relax travel restrictions, and reopen borders as they return to normality. A large proportion of the world’s major aviation markets with originating passenger traffic have reached vaccination rates of 80%. In many cases, vaccines serve as a passport to travel in the current context.

Downside risks

- Geopolitical conflicts

The conflict between Russia and Ukraine further damaged the global economy disrupting trade and driving a slowdown in 2022. It not only triggered a rise in energy prices affecting the cost of travel but also a humanitarian crisis resulting in millions of refugees and a global food crisis. There are risks of worldwide spillovers to other commodity markets adding to inflation pressures.

- Economic downturn

The risk for an economic downturn due to rising interest rates aimed at curbing inflation is ever present. Coupled with the significant increase in jet fuel prices, this could weaken and even delay the aviation industry recovery in the short-term by increasing the cost of travel. The IMF expects inflation to remain in 2022, projected to reach 6.6% in advanced economies and 9.5% in emerging markets and developing economies[1]. Central banks continue to increase interest rates in order to tame inflation—this will potentially contract or slow the growth of economic output.

- Supply chain bottlenecks and labour shortage

Supply chain disruption affecting a large range of commodities and services triggered a rapid rise in the price of oil and gas—including jet fuel—as well as a broader transportation crisis. The shortage of shipping containers, clogged seaports and cross-border shipment disruptions have a direct impact on the health of the global economy. The air transport sector is especially affected by labour shortages across all players in the aviation ecosystem.

Despite the downside risks, the industry remains confident that the potential for a recovery to 2019 levels within two or three years is possible assuming a short-lived recession in 2023. There is no doubt that many people remain eager to resume travelling and the 2022 early Northern Hemisphere summer volumes are a testament to that. With the combination of vacation deprivation and an upsurge in confidence in air travel provided by increased vaccination rates and safety measures, the relaxation of travel restrictions will help boost the propensity for air travel and fuel the industry’s recovery.

Based on the points above, the 2022 Q3 and Q4 projections are as follows:

World

- Global passenger traffic in the year 2022 is expected to be 6.8 billion, representing a loss of 33.1% compared to the projected baseline, which is 74.4% of 2019 traffic.

- Full recovery to 2019 levels at the global level is forecast for 2024.

Africa

- The region is expected to reach close to 79.3% of its 2019 level in the year 2022.

- Due to its dependence on international traffic,Africa will remain part of the highly impacted regions and is expected to make a full recovery to 2019 levels only in mid- to late 2024.

Asia-Pacific

- While some countries in Asia-Pacific have reopened to vaccinated travelers, the international passenger market is not expected to see significant improvement before the second half of 2022. The region is expected to have the slowest recovery, reaching only 54.5% of 2019 levels in 2022.

- Full year recovery to 2019 levels is expected by the end of 2024 but could slip into 2025 if some countries lag to lift the remaining COVID-19 restrictions.

Europe

- With the significant improvement in the first half of the year 2022, the region in the year 2022 will mark 82.5% of its 2019 level.

- Despite some risks of a slowdown during the fall and winter seasons, Europe full-year recovery to 2019 levels is expected in 2024.

Latin America-Caribbean

- The region is expected to continue seeing a positive uptick in 2022. The increase in leisure travel is forecast to bring the region to 91.9% compared to 2019.

- Full-year recovery for the region is expected in late 2023.

The Middle East

- With the region’s high dependence on international travel and connectivity, both of which are improving in Europe and Asia-Pacific except China, the region will continue to boost its recovery in 2022.

- The region is expected to reach 82.7% of 2019 levels by year end and fully recover only in the first half of 2024.

North America

- The strong performance is expected to continue in 2022, helping the region to reach 89.6% of its 2019 level by year end.

- North America should be the first region to reach full-year recovery to 2019 levels as early as in 2023.

Chart 3: Medium-term global passenger traffic projection (indexed, 2019 = 100)

* The pre-COVID-19 forecast scenario is based on a standard time-series forecast generated using the most up-to-date and complete historical data to December 2019. It also makes use of an adjusted World Airport Traffic Forecasts (WATF) 2019–2040 and considers the latest insights provided by ACI Regional offices and other inputs.

** Estimated passenger traffic volumes scenarios (current projection and pessimistic) are based on a broad range of inputs provided by ACI Regional offices and industry experts.

Source: ACI World

Chart 4: Medium-term global passenger traffic by type (in billion passengers)

Source: ACI World

Under those assumptions, ACI World forecasts the following regarding the recovery of airport passenger traffic:

- Under the current projection, accounting for the faster than expected first and second quarters of 2022 despite the Omicron wave, global passenger traffic is expected to reach 2019 levels in late 2023 with the full-year recovery to 2019 levels in 2024. The overall recovery will mainly be driven by the recovery of domestic passenger traffic but may be hampered by stagnation in Asia-Pacific and a slower recovery in global international travel (globally, domestic traffic accounted for 58% of total passenger traffic in 2019).

- Global domestic passenger traffic is still expected to reach its 2019 level in late 2023 with full-year 2023 traffic on par with the 2019 level. However, global international passenger traffic will require almost one more year to recover and will reach its 2019 high only in the second half of 2024. Full-year recovery to 2019 levels will only happen in 2025 for international passenger traffic.

- At the country-market level, markets having significant domestic traffic are expected to recover to pre-COVID-19 levels in the second half of 2023. Some heavily restricted markets are unlikely to return to 2019 levels until 2024, with some having to wait until 2025. Due to the uneven availability of vaccines, geopolitical conflict, and the resulting humanitarian crisis, not to mention the worsening economic outlook, some country-markets—especially emerging and developing economies—will probably not reach 2019 passenger levels before 2025 or 2026, especially those markets reliant on international traffic.

[1] International Monetary Fund. World Economic Outlook Update. Gloomy and More Uncertain. July 2022

About ACI World

Airports Council International (ACI), the trade association of the world’s airports, was founded in 1991 with the objective of fostering cooperation among its member airports and other partners in world aviation, including the International Civil Aviation Organization, the International Air Transport Association, and the Civil Air Navigation Services Organization. In representing the best interests of airports during key phases of policy development, ACI makes a significant contribution toward ensuring a global air transport system that is safe, secure, efficient, and environmentally sustainable. As of January 2022, ACI serves 717 members, operating 1950 airports in 185 countries.

https://aci.aero/2022/10/06/the-impact-of-covid-19-on-airports-and-the-path-to-recovery/