Let me to summary all my findings

NAV = 30 , regular profit last year = 14.3 Mn ,

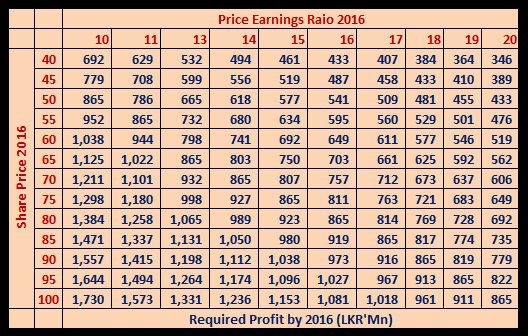

shares = 78,653,255 , W18 = 31,461,302 W19 = 62,922,604

Total shares when all the warrants get converted (if) = 173,037,161

Total money comes from warrants = 3.46Bn

Future earnings

Irregular Gains

Profits (based on NAV change) from listing Kalpitiya and Waskaduwa = 78.88 + 22.05 = 101Mn

Transfer gain , Hikkaduwa Land = 72Mn {366 (transferred) -294(book)

Hikkaduwa PP gain = 109 Mn (NAV will be 13. shares 36Mn *3 )

Total possible gain this year = 280Mn

Future possible gains

Leasing 50 villas in Kalpitiya - profit = 937Mn (Pros of Kal)

Selling CLND stake : average cost per share = 31.5

Listing Hikkaduwa

Passikudah (Land transfer, PP , Listing)

Regular earnings

From every subsidiary hotel REEF expecting a management fees. 3% of the Rev + 2% gross profit

Kalpitiya estimated Rev in 2018 = 1bn Gross profit around 700Mn

Estimated annual management fees from Kalpitiya = 46Mn

Waskaduwa = 46Mn

Hikkaduwa = 23Mn

Possible management fees from all the subs (Kalpitiya, Waskaduwa, Hikkaduwa, Passikudah, ... ) = more than 200 Mn

Profit share from regular hotel operations = ???

Citrus Leisure @2016

Citrus Hikkaduwa ( 92 rooms )

Citrus Waskaduwa (150) + 50 Villas

Citrus Kalpitiya (150)

Citrus Passikudah (50 villas initially)

Citrus Hambantota with 200 rooms (??? . on card)

Last edited by sapumal on Wed Jan 25, 2012 3:06 pm; edited 1 time in total

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*