Thanks Chinwi. This will useful for my further analysis

Chinwi wrote:

Please Note I did not intend to promote this share. Now I feel I have talked too much about this.

Greedy,

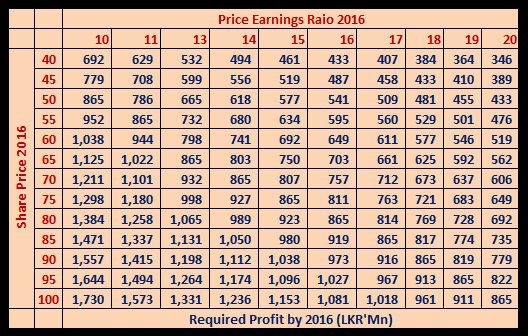

The following is also reproduced from REEF cash flow forecast sent to us last year. .

Year 2016

Room nights 164,250

Room rate 160 Us$ (avr)

Revenue 2,487,340,134.00 ( Exchange Rate 116.00)

F&B Rev 2,035,000,000.00

Total Revenue 4,522,436,607.00

Direct Costs 904,487,321.00

Opr. Expences 994,936,054.00

Total Expenditure 1,899,423,375.00

Operational Profit 2,623,013,232.00 ( 2.623 billioin)

just the forecast.

Hoping we are going to hit exchange rate of 120 in near future. Basil also put pressure on Cabral.

seyon wrote:Very good analyis and discussion, I am also following this share after spotted by smallville.

Next warrants is going to be converted on May 2012 ( I guess) So we have to wait and see the trend of the shares and warrants during the conversion. that would give some input for our analysis interms of price trend shareholding structure.

Thanks for the analysis.

Interesting person in the list is Tharana Gangul . Very close person to නිමල්, ධම්මික, CEO and director of RCL

He didn't had much warrants(1Mn) . But from 2010/12/30 to 2011/9/30 he has bought further 4Mn warrants (W18). Average cost may be over 25. He is one who know about REEF future (may be for trading purposes).

Director of RCL

RCL invested on REEF

RCL has connection with නිමල් පෙරෙරා

නිමල් , දිලිත, Amunumaga close persons

Also we thought when DP sold reef @45 it is very much over valued (15.7 Mn shares). But when it released the quarter report on 2011 March we can assume it is fairly valued

Profit for 3 months = 14.3Mn

EPS = .91

Annualized EPS = 3.65

PE = 12.3

With the increase of tourist arrival and increased room charges profit of 57Mn (PE = 12.3 ) hadn't been a very difficult achievement.

But they chose to expand.

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*