would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

Bartleet Religare Securities says.

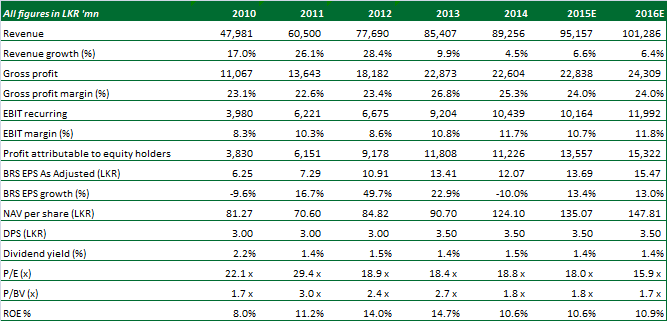

We have revised downwards our long-term growth forecasts along with a split valuation for the gaming project and the hotel property. We value the existing business at LKR 231, and including the earnings of the WFP (minus the gaming aspect to remove political/legislative risk: safer scenario) at LKR 249. With the inclusion of the casino project, we have valued the group at LKR 288. Despite unrivalled share liquidity in the CSE, we believe the CMP makes the valuations relatively expensive for both the existing business and for the WFP given the time value. The Warrants appear to offer cheaper exposure to JKH in the medium term.

" />

" />

We have revised downwards our long-term growth forecasts along with a split valuation for the gaming project and the hotel property. We value the existing business at LKR 231, and including the earnings of the WFP (minus the gaming aspect to remove political/legislative risk: safer scenario) at LKR 249. With the inclusion of the casino project, we have valued the group at LKR 288. Despite unrivalled share liquidity in the CSE, we believe the CMP makes the valuations relatively expensive for both the existing business and for the WFP given the time value. The Warrants appear to offer cheaper exposure to JKH in the medium term.

" />