would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

Moving up the value chain – STRONG BUY

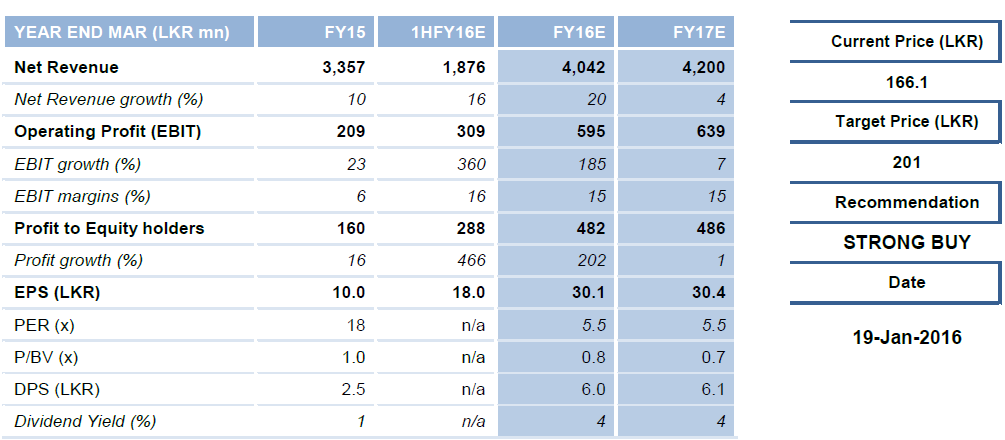

BFL, one of the leading poultry firms in Sri Lanka, recorded a 10% YoY growth in FY15 net revenue, while profit increased 16% YoY to LKR 160mn. CAL expects BFL to post a net revenue Cagr of 11% over FY15-19E as per capita chicken consumption increases at a Cagr of 8% through 2019E. Further, BFL is currently in the process of constructing its own feed mill which will make it a fully integrated poultry firm and is expected to come online by FY17E. As a result, CAL expects a reduction in BFL’s Feed Conversion Ratio (FCR) to 1.6x by FY19E from the current 1.8x. This is expected to translate into an EPS Cagr of 51% over FY15-19E. CAL’s DCF value for BFL is LKR 201, representing a share price upside of 21% and a total return of 25% (dividend yield of 4%). STRONG BUY

BFL, one of the leading poultry firms in Sri Lanka, recorded a 10% YoY growth in FY15 net revenue, while profit increased 16% YoY to LKR 160mn. CAL expects BFL to post a net revenue Cagr of 11% over FY15-19E as per capita chicken consumption increases at a Cagr of 8% through 2019E. Further, BFL is currently in the process of constructing its own feed mill which will make it a fully integrated poultry firm and is expected to come online by FY17E. As a result, CAL expects a reduction in BFL’s Feed Conversion Ratio (FCR) to 1.6x by FY19E from the current 1.8x. This is expected to translate into an EPS Cagr of 51% over FY15-19E. CAL’s DCF value for BFL is LKR 201, representing a share price upside of 21% and a total return of 25% (dividend yield of 4%). STRONG BUY