would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

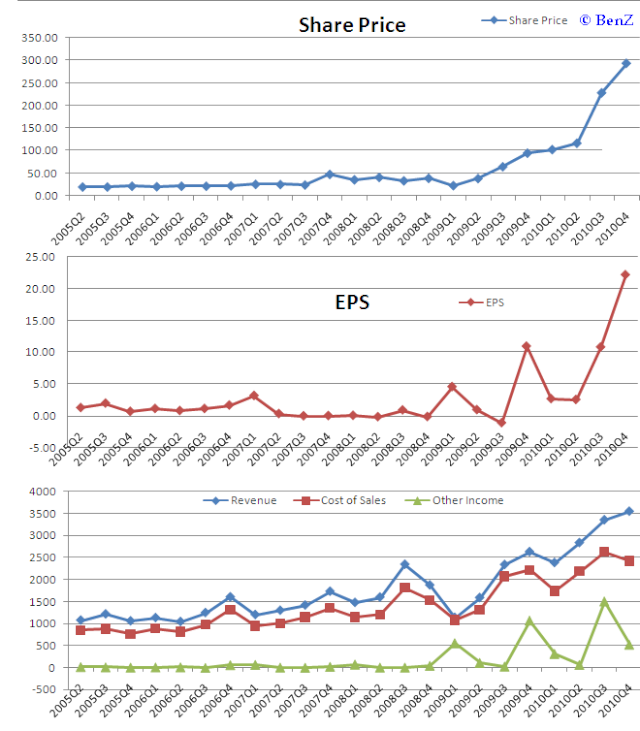

A small analysis of BRWN;

Current Assets = 7823.78Mn

Current Liabilities = 4740.4Mn

Hence positive working capital.

Share holders equity as at 31-12-10 = 12070Mn

Revenue = 9749 Mn

Other Income = 2519.5 Mn (could not find any related data)

-----------------------------

Equity Holders = 2523.56 Mn

-----------------------------

Annualized Equity Holders = 2523.56/3*4 = 3364.75Mn

Announced EPS for 9 months = 35.61

Ordinary Shares = 70.875 Mn

Calculated Annualised EPS = 3364.75/70.875 = 47.47

Trading sector PE = 9.10

Sector Valuation - 47.47*9.10 = 431.98/-

Current Price = 380/-

Current PE = 380/47.47 = 8.0

Current ROE = 2523.56/12070 = 20.9%

Looks very under valued to me..

Browns Future plans include entering areas such as; Forestry, Hotels & Eco-tourism and Real estate development. This would eventually result in additional revenue being generated for the company. Also Galoya plantations project can be considered as a future investment as it will start suger production in 2011. The PP which raised 4.1 Bn rupees also included in cash flows.

Since Last Qtr profits = 1219.1 Mn, if we take the growth rate as 10% over the qtr = 1341 Mn. Then the Annulaised earnings would be 3864.57.

Then the projected EPS = 3864.57/70.875 = 54.53.

Hence Projected valuation over a 10% qtr PAT growth = 496.2/-

But the only problem I found was to identify the other income figure, cuz if we take it out.. theres nothing much as a gain..

But this is a good med-long term hold considering the growth of the company and industry as well.

Current Assets = 7823.78Mn

Current Liabilities = 4740.4Mn

Hence positive working capital.

Share holders equity as at 31-12-10 = 12070Mn

Revenue = 9749 Mn

Other Income = 2519.5 Mn (could not find any related data)

-----------------------------

Equity Holders = 2523.56 Mn

-----------------------------

Annualized Equity Holders = 2523.56/3*4 = 3364.75Mn

Announced EPS for 9 months = 35.61

Ordinary Shares = 70.875 Mn

Calculated Annualised EPS = 3364.75/70.875 = 47.47

Trading sector PE = 9.10

Sector Valuation - 47.47*9.10 = 431.98/-

Current Price = 380/-

Current PE = 380/47.47 = 8.0

Current ROE = 2523.56/12070 = 20.9%

Looks very under valued to me..

Browns Future plans include entering areas such as; Forestry, Hotels & Eco-tourism and Real estate development. This would eventually result in additional revenue being generated for the company. Also Galoya plantations project can be considered as a future investment as it will start suger production in 2011. The PP which raised 4.1 Bn rupees also included in cash flows.

Since Last Qtr profits = 1219.1 Mn, if we take the growth rate as 10% over the qtr = 1341 Mn. Then the Annulaised earnings would be 3864.57.

Then the projected EPS = 3864.57/70.875 = 54.53.

Hence Projected valuation over a 10% qtr PAT growth = 496.2/-

But the only problem I found was to identify the other income figure, cuz if we take it out.. theres nothing much as a gain..

But this is a good med-long term hold considering the growth of the company and industry as well.