would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

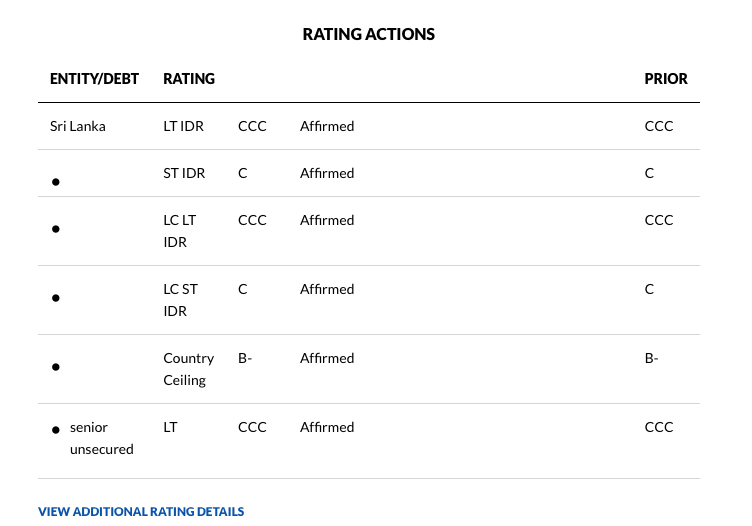

Fitch Ratings - Hong Kong - 14 Jun 2021: Fitch Ratings has affirmed Sri Lanka's Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'CCC'.

KEY RATING DRIVERS

Sri Lanka's 'CCC' rating reflects a challenging foreign-currency sovereign external debt repayment burden over the medium term, low foreign-exchange reserves and high and rising government debt that gives rise to sustainability risks.

External liquidity pressures have eased somewhat in recent months following bilateral loan disbursements, and our expectation of a forthcoming IMF special drawing rights (SDR) allocation. Nevertheless, Sri Lanka's medium-term debt service challenges are substantial and pose risks to the sovereign's debt repayment capacity, in Fitch's view. A total of about USD29 billion in foreign-currency debt obligations are due between now and 2026, against foreign-exchange reserves of USD4.5 billion as of end-April 2021.

The authorities have recently secured project financing through various multilateral and bilateral channels, including the Asian Development Bank (AAA/Stable), Asian Infrastructure Investment Bank (AAA/Stable), China Development Bank (A+/Stable) and The Export-Import Bank of Korea (AA-/Stable), as well as swap facilities under the South Asian Association for Regional Cooperation (SAARC) currency framework and the People's Bank of China, equivalent to USD400 million and USD1.5 billion, respectively. The planned IMF SDR allocation would also add USD780 million to reserves. These resources should enable Sri Lanka to meet its remaining debt maturities through the rest of this year, including a USD1 billion International Sovereign Bond maturing in July. However, the authorities have yet to specify their plans for meeting the country's foreign-currency debt-servicing needs for 2022 and the medium term. They have consistently indicated that they do not plan to seek programme financing from the IMF.

We project foreign-exchange reserves to remain at about USD 4.5 billion by end-2021 before declining to USD3.9 billion by end-2022. Under our baseline, the current account deficit is likely to widen to 2.8% in 2021 and narrow to 2.1% of GDP in 2022. Our forecasts assume remittances will remain resilient in 2021-2022 and tourism is likely to recover only from 2022.

Sri Lanka's economy contracted by 3.6% in 2020 as a result of the Covid-19 pandemic. We project growth of 3.8% in 2021, down from an earlier forecast of 4.9%, in light of a recent surge in virus cases. We expect the economy to grow by 3.9% in 2022. There remains a high degree of uncertainty associated with our forecasts in light of the evolution of new Covid-19 cases in the country. The authorities plan to inoculate 60% of the population by end-2021, but this target could be hampered by vaccine supply shortages.

Travel and tourism, an important driver of the economy, have been hit hard and the outlook for recovery remains uncertain, particularly given the recent surge in virus cases. The direct contribution of tourism to pre-pandemic GDP was about 4%, but the indirect contribution was much higher. Tourist arrivals in the first five months of 2021 were 97% lower than the same period last year.

The general government deficit widened to 11.1% of GDP in 2020, from 9.6% in 2019, as the economic contraction led to a sharp fall in fiscal revenue. We expect the deficit to remain elevated in 2021 and 2022 at 11.1% and 10.4%, respectively. Our deficit projections are wider than those presented by the government under its growth-oriented strategy of 9.4% and 7.5%, respectively. Under our forecasts, the revenue-to-GDP ratio in 2021 would rise to 10.9% in 2021 and 11.1% in 2022, compared with the authorities' projections of 11.9% and 13.0%, respectively.

The government's fiscal consolidation strategy is based on a planned acceleration in GDP growth, underpinned by tax cuts, as opposed to direct revenue-raising or expenditure measures, albeit supported by planned improvements in tax administration. The interest-to-revenue ratio remains high, at around 71% as of 2020, well above the 'CCC' median of 13%. The government expects to achieve primary surpluses from 2023, supported by annual GDP growth of 6%, which appear optimistic in our view as we anticipate growth that is closer to 4%, still above the pace in the immediate pre-pandemic period.

General government debt reached 101% of GDP by end-2020, broadly in line with our forecast at our last review in November. Our baseline forecasts suggest this ratio will rise further to 108% by 2022. Fitch does not think the government will meet its 2025 targets of reducing government debt to 70% of GDP and narrowing the fiscal deficit to 4% of GDP.

Sri Lanka's basic human development indicators, including education standards, are high compared with those of rating category peers. The UN Human Development Index Score positions Sri Lanka in the 62nd percentile, well above the 27th percentile for the 'CCC' median. The country's per capita income of about USD3,822 is also above the 'CCC' median of USD2,662.

The banking sector is vulnerable to Sri Lankan sovereign weakness due to the banks' significant direct exposure to the sovereign and their domestically focused operations. The operating environment for banks remains challenging, and asset quality continues to be a key risk. Reported asset-quality measures at end-2020 - impaired loans for Fitch-rated banks rose to 9.7% by end-2020 from 9.5% at end-2019 -- likely understate the extent of credit impairment due to forbearance measures.

ESG - Governance: Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights as well as for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption, as is the case for all sovereigns. These scores reflect the high weight that the World Bank Governance Indicators have in our proprietary Sovereign Rating Model. Sri Lanka has a medium World Bank Governance Indicator ranking in the 46th percentile, reflecting a recent record of peaceful political transitions, a moderate level of rights for participation in the political process, moderate institutional capacity, established rule of law and a moderate level of corruption.

RATING SENSITIVITIES

FACTORS THAT COULD, INDIVIDUALLY OR COLLECTIVELY, LEAD TO NEGATIVE RATING ACTION/DOWNGRADE:

- Increased signs of a probable default event, for instance, from severe external liquidity stress, potentially reflected in an ongoing erosion of foreign-exchange reserves and reduced capacity of the government to access external financing.

FACTORS THAT COULD, INDIVIDUALLY OR COLLECTIVELY, LEAD TO POSITIVE RATING ACTION/UPGRADE:

-External Finances: Improvement in external finances, supported by higher non-debt inflows or a reduction in external sovereign refinancing risks from an improved liability profile.

- Public Finances: Stronger public finances, reflected in a sustained decline in the general government debt-to-GDP ratio to closer to the 'B' median, and underpinned by a credible medium-term fiscal consolidation strategy.

- Structural: Improved policy coherence and credibility, leading to more sustainable public and external finances and a reduction in the risk of debt distress.

SOVEREIGN RATING MODEL (SRM) AND QUALITATIVE OVERLAY (QO)

In accordance with the rating criteria for ratings in the 'CCC' range and below, Fitch's sovereign rating committee has not used the SRM and QO to explain the ratings, which are instead guided by our rating definitions.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a Long-Term Foreign-Currency Issuer Default Rating. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Sovereigns, Public Finance and Infrastructure issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of three notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit https://www.fitchratings.com/site/re/10111579.

KEY ASSUMPTIONS

The global economy performs in line with Fitch's global GDP forecasts published in the latest Global Economic Outlook report.

KEY RATING DRIVERS

Sri Lanka's 'CCC' rating reflects a challenging foreign-currency sovereign external debt repayment burden over the medium term, low foreign-exchange reserves and high and rising government debt that gives rise to sustainability risks.

External liquidity pressures have eased somewhat in recent months following bilateral loan disbursements, and our expectation of a forthcoming IMF special drawing rights (SDR) allocation. Nevertheless, Sri Lanka's medium-term debt service challenges are substantial and pose risks to the sovereign's debt repayment capacity, in Fitch's view. A total of about USD29 billion in foreign-currency debt obligations are due between now and 2026, against foreign-exchange reserves of USD4.5 billion as of end-April 2021.

The authorities have recently secured project financing through various multilateral and bilateral channels, including the Asian Development Bank (AAA/Stable), Asian Infrastructure Investment Bank (AAA/Stable), China Development Bank (A+/Stable) and The Export-Import Bank of Korea (AA-/Stable), as well as swap facilities under the South Asian Association for Regional Cooperation (SAARC) currency framework and the People's Bank of China, equivalent to USD400 million and USD1.5 billion, respectively. The planned IMF SDR allocation would also add USD780 million to reserves. These resources should enable Sri Lanka to meet its remaining debt maturities through the rest of this year, including a USD1 billion International Sovereign Bond maturing in July. However, the authorities have yet to specify their plans for meeting the country's foreign-currency debt-servicing needs for 2022 and the medium term. They have consistently indicated that they do not plan to seek programme financing from the IMF.

We project foreign-exchange reserves to remain at about USD 4.5 billion by end-2021 before declining to USD3.9 billion by end-2022. Under our baseline, the current account deficit is likely to widen to 2.8% in 2021 and narrow to 2.1% of GDP in 2022. Our forecasts assume remittances will remain resilient in 2021-2022 and tourism is likely to recover only from 2022.

Sri Lanka's economy contracted by 3.6% in 2020 as a result of the Covid-19 pandemic. We project growth of 3.8% in 2021, down from an earlier forecast of 4.9%, in light of a recent surge in virus cases. We expect the economy to grow by 3.9% in 2022. There remains a high degree of uncertainty associated with our forecasts in light of the evolution of new Covid-19 cases in the country. The authorities plan to inoculate 60% of the population by end-2021, but this target could be hampered by vaccine supply shortages.

Travel and tourism, an important driver of the economy, have been hit hard and the outlook for recovery remains uncertain, particularly given the recent surge in virus cases. The direct contribution of tourism to pre-pandemic GDP was about 4%, but the indirect contribution was much higher. Tourist arrivals in the first five months of 2021 were 97% lower than the same period last year.

The general government deficit widened to 11.1% of GDP in 2020, from 9.6% in 2019, as the economic contraction led to a sharp fall in fiscal revenue. We expect the deficit to remain elevated in 2021 and 2022 at 11.1% and 10.4%, respectively. Our deficit projections are wider than those presented by the government under its growth-oriented strategy of 9.4% and 7.5%, respectively. Under our forecasts, the revenue-to-GDP ratio in 2021 would rise to 10.9% in 2021 and 11.1% in 2022, compared with the authorities' projections of 11.9% and 13.0%, respectively.

The government's fiscal consolidation strategy is based on a planned acceleration in GDP growth, underpinned by tax cuts, as opposed to direct revenue-raising or expenditure measures, albeit supported by planned improvements in tax administration. The interest-to-revenue ratio remains high, at around 71% as of 2020, well above the 'CCC' median of 13%. The government expects to achieve primary surpluses from 2023, supported by annual GDP growth of 6%, which appear optimistic in our view as we anticipate growth that is closer to 4%, still above the pace in the immediate pre-pandemic period.

General government debt reached 101% of GDP by end-2020, broadly in line with our forecast at our last review in November. Our baseline forecasts suggest this ratio will rise further to 108% by 2022. Fitch does not think the government will meet its 2025 targets of reducing government debt to 70% of GDP and narrowing the fiscal deficit to 4% of GDP.

Sri Lanka's basic human development indicators, including education standards, are high compared with those of rating category peers. The UN Human Development Index Score positions Sri Lanka in the 62nd percentile, well above the 27th percentile for the 'CCC' median. The country's per capita income of about USD3,822 is also above the 'CCC' median of USD2,662.

The banking sector is vulnerable to Sri Lankan sovereign weakness due to the banks' significant direct exposure to the sovereign and their domestically focused operations. The operating environment for banks remains challenging, and asset quality continues to be a key risk. Reported asset-quality measures at end-2020 - impaired loans for Fitch-rated banks rose to 9.7% by end-2020 from 9.5% at end-2019 -- likely understate the extent of credit impairment due to forbearance measures.

ESG - Governance: Sri Lanka has an ESG Relevance Score of '5' for Political Stability and Rights as well as for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption, as is the case for all sovereigns. These scores reflect the high weight that the World Bank Governance Indicators have in our proprietary Sovereign Rating Model. Sri Lanka has a medium World Bank Governance Indicator ranking in the 46th percentile, reflecting a recent record of peaceful political transitions, a moderate level of rights for participation in the political process, moderate institutional capacity, established rule of law and a moderate level of corruption.

RATING SENSITIVITIES

FACTORS THAT COULD, INDIVIDUALLY OR COLLECTIVELY, LEAD TO NEGATIVE RATING ACTION/DOWNGRADE:

- Increased signs of a probable default event, for instance, from severe external liquidity stress, potentially reflected in an ongoing erosion of foreign-exchange reserves and reduced capacity of the government to access external financing.

FACTORS THAT COULD, INDIVIDUALLY OR COLLECTIVELY, LEAD TO POSITIVE RATING ACTION/UPGRADE:

-External Finances: Improvement in external finances, supported by higher non-debt inflows or a reduction in external sovereign refinancing risks from an improved liability profile.

- Public Finances: Stronger public finances, reflected in a sustained decline in the general government debt-to-GDP ratio to closer to the 'B' median, and underpinned by a credible medium-term fiscal consolidation strategy.

- Structural: Improved policy coherence and credibility, leading to more sustainable public and external finances and a reduction in the risk of debt distress.

SOVEREIGN RATING MODEL (SRM) AND QUALITATIVE OVERLAY (QO)

In accordance with the rating criteria for ratings in the 'CCC' range and below, Fitch's sovereign rating committee has not used the SRM and QO to explain the ratings, which are instead guided by our rating definitions.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a Long-Term Foreign-Currency Issuer Default Rating. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

BEST/WORST CASE RATING SCENARIO

International scale credit ratings of Sovereigns, Public Finance and Infrastructure issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of three notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from 'AAA' to 'D'. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit https://www.fitchratings.com/site/re/10111579.

KEY ASSUMPTIONS

The global economy performs in line with Fitch's global GDP forecasts published in the latest Global Economic Outlook report.