would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

would enable you to enjoy an array of other services such as Member Rankings, User Groups, Own Posts & Profile, Exclusive Research, Live Chat Box etc..

Latest*

Latest*

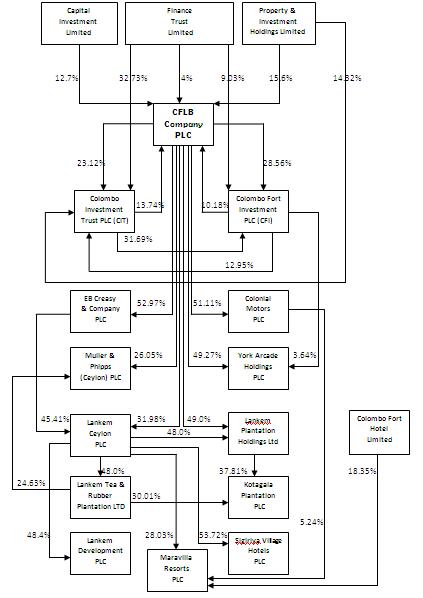

The Colombo Fort Land & Building PLC is engaged in real estate and property development, management of an investment portfolio and the provision of management services. The Company operates in five segments: Trading of Consumer Products, Trading of Industrial Products, Leisure, Plantations and Others. The Company, through its subsidiaries, is engaged in manufacturing and marketing of chemicals, paints, hardware, building materials and packaging; manufacturing and marketing of consumer disposables, food and beverage products; marketing and distribution of pharmaceuticals; marketing of motor vehicles and accessories, and the provision of vehicle maintenance services. In addition, the Company involves in the operation of tourist hotels and inbound tour operations; production, processing and marketing of tea, rubber and desiccated coconut, and management of investment portfolios. Its subsidiaries include Agarapatana Plantations Limited, Kotagala Plantations PLC and Marawila Resorts PLC.

CFLB prices have gone up so much, there is a rumor in the market that there is a rights issue or split. Is it true? do you think it is worth buying this company at this price. Also what do you think of lankem and cw mackie.

CFLB prices have gone up so much, there is a rumor in the market that there is a rights issue or split. Is it true? do you think it is worth buying this company at this price. Also what do you think of lankem and cw mackie.

Last edited by CHRONICLE™ on Sat Jun 05, 2021 3:00 pm; edited 1 time in total